Asset Valuations

Asset Depreciation and Valuations

Fixed assets have a fixed lifetime. Depreciation is the difference between the cost of buying an asset and any proceeds that will be gained upon disposal. Depreciation is the part of the cost of the fixed asset consumed during its period of use. Depreciation is an expense and is charged to the profit and loss account.

SmartTraxx assists in the management of original cost, replacement cost and actual cash value for all capital assets, based on an organizations requirements and integration with backend systems like Oracle or SAP. SmartTraxx also assists in management of surplus valuations and actual (disposal) value based on an asset’s selling price at time of final disposal.

SmartTraxx manages the status of assets and the passage of time, to determine the real-time value of assets. Asset valuations from SmartTraxx sync with an organizations backend software systems and general ledger.

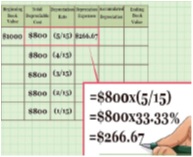

Depreciation is a method of reallocating the cost of a tangible asset over its useful life span of it being in motion. Businesses depreciate long-term assets for both tax and accounting purposes. The former affects the balance sheet of a business or entity, and the latter affects the net income that they report. Generally the cost is allocated, as depreciation expense, among the periods in which the asset is expected to be used. This expense is recognized by businesses for financial reporting and tax purposes. Methods of computing depreciation, and the periods over which assets are depreciated, may vary between asset types within the same business and may vary for tax purposes. These may be specified by law or accounting standards, which may vary by country. There are several standard methods of computing depreciation expense, including fixed percentage, straight line, and declining balance methods. Depreciation expense generally begins when the asset is placed in service. For example, a depreciation expense of $100 per year for five years may be recognized for an asset costing $500.

While depreciation expense is recorded on the income statement of a business, its impact is generally recorded in a separate account and disclosed on the balance sheet as accumulated depreciation, under fixed assets, according to most accounting principles.